The Missing Piece of Your AI Strategy: Distribution

How to navigate the new AI ecosystem to reach your target customers

The past three decades have taught a simple truth: the best product rarely wins on its own. In the 1990s, the coolest websites without distribution vanished. In mobile, countless apps out-innovated peers only to be crushed by those who secured App Store placement, carrier deals, or platform integration. Generative AI is no different.

AI isn’t adopted in isolation. It’s discovered through marketplaces, embedded in workflows, routed through consulting programs, bundled into IT upgrades, remixed in communities, or disguised as data inside trusted incumbents.

A great product and a sales force aren’t enough. As Stratechery’s The AI Unbundling argued, AI’s value chain may start with model creation, but power shifts downstream — toward whoever controls distribution and consumption.

Distribution — not innovation — will separate winners from losers.

Look at SEO today: if your brand isn’t surfacing in Google Gemini’s instant answers, you may as well not exist. The same applies in enterprise — if your SaaS product isn’t on AWS Marketplace or embedded in Salesforce, you’re invisible when buying decisions get made.

In the AI era, go-to-market strategy is distribution strategy. Companies must either own the distribution platform or scale through someone else’s. Only a handful of players — like OpenAI, Google, Meta, and Amazon — truly own distribution. Everyone else needs to master how to ride it.

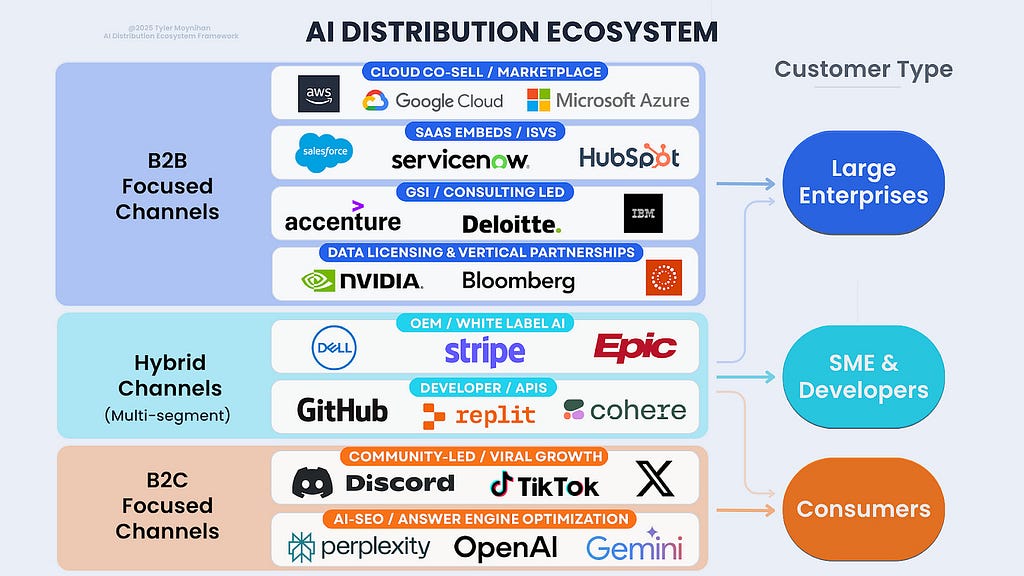

This article lays out eight key distribution strategies. For each, I explain how it works, which companies it fits, and illustrate it with a real-world case study. These channels fall into three groups: enterprise, hybrid, and consumer.

The lesson is consistent: innovation gets you noticed, distribution gets you scaled.

Enterprise-Focused Channels

1. Cloud Co-Sell & Marketplaces

Best For: B2B SaaS and AI companies targeting enterprise customers and looking to shorten procurement cycles.

In enterprise sales, great demos rarely kill a deal — procurement does. Security reviews and vendor approvals can stretch sales cycles from months to years. Cloud marketplaces (like AWS, Azure, and GCP) flip that script by turning procurement itself into a distribution engine.

Think of them as digital storefronts where enterprises buy software through their existing cloud accounts. Instead of becoming a new vendor that has to clear security and budget hurdles, listing your product on a marketplace makes it part of a pre-approved contract and spend.

This is further amplified through co-sell, where cloud provider reps actively help sell your product because when you win, they hit their own sales targets too. In effect, the cloud stops being just infrastructure and becomes a highly leveraged sales channel.

This isn’t a niche strategy. Recent research shows that about 70% of software vendors now sell through cloud marketplaces, and major resellers like CDW and SHI use special cloud programs to bundle AI tools into standard IT upgrades — so adoption happens almost automatically.

Case Study: Databricks → AWS.

Databricks had strong enterprise demand but long procurement cycles. Listing its Data Intelligence Platform on AWS Marketplace changed the game. Customers could use AWS credits, and reps co-sold Databricks to hit their own numbers.

Marketplace sales quadrupled, average deal size doubled, and Databricks says its AWS marketplace business surpassed a $1B run rate. Distribution turned a bottleneck into a growth engine.

Keys to Success:

- Treat marketplaces as sales engines, not just shelves.

- Pre-build private offers so deals close instantly with credits.

- Co-map accounts with AWS/Azure/GCP reps so your wins drive theirs.

2. SaaS Embeds / ISVs

Best For: AI tools that add the most value inside existing workflows.

Most AI tools fail when they sit outside daily workflows. Embedding into established SaaS platforms turns your product into a native feature, cutting friction and accelerating adoption. Salesforce, ServiceNow, Microsoft 365, HubSpot aren’t just apps — they’re distribution rails.

As Notion Capital puts it: “AI isn’t bought, it’s adopted.” Adoption happens fastest when intelligence shows up inside trusted workflows. Many platforms call partners “ISVs” (independent software vendors), but the label matters less than the outcome: your AI becomes part of the system.

Case Study: Grammarly → Google Docs.

Grammarly gained mass adoption not just through its standalone app, but by embedding directly into Google Docs and Microsoft 365, where users were already writing. Instead of asking users to switch tools, Grammarly showed up exactly where they worked. That workflow embed transformed it from a consumer product into a default layer of enterprise writing infrastructure.

Keys to Success:

- Make installation one-click and self-serve.

- Ship templates and recipes, not just APIs.

- Win over platform architects — they decide which integrations thrive.

3. GSI / Consulting-Led Distribution

Best For: Enterprise AI solutions needing governance, organizational change, or regulatory clearance.

Global system integrators (GSIs) like Accenture, Deloitte, PwC, and Capgemini don’t sell tools — they sell transformation. By embedding AI into their modernization programs, you gain access to enterprises that might otherwise hesitate. Customers don’t buy “an AI product”; they buy a roadmap from a trusted partner.

Research shows much of AI adoption in regulated industries flows through GSIs, not direct deals. As one investor said: “Accenture can get you into a hundred enterprises faster than a hundred AEs — if you package yourself as part of their transformation stack.”

Case Study: Anthropic → Deloitte.

Deloitte formed a strategic alliance with Anthropic to bring Claude-powered assistants into regulated enterprise programs. Deloitte packages the tech into transformation offerings, so clients feel they’re buying a roadmap, not a tool.

Keys to Success:

- Package AI into repeatable “solution kits.”

- Land one flagship deployment and use it as a reference.

- Accept long cycles; once embedded, scale comes fast.

4. Data Licensing & Vertical AI Partnerships

Best For: AI in regulated, IP-heavy, or trust-dependent industries.

In verticals like healthcare, finance, and media, trust and governance drive adoption.

Here, AI scales by embedding through incumbents who own distribution and credibility. Your tech powers outcomes, but the trusted partner owns the customer.

Case Study: Getty Images → NVIDIA.

Rather than race to build its own generative model, Getty leaned into its rights-cleared library. In 2023, it licensed its content to NVIDIA for training foundation models.

For Getty, this unlocked new AI revenue without competing directly. For NVIDIA, it provided legally safe training data. Distribution came through licensing into one of the most powerful AI platforms in the world.

Keys to Success:

- Lead with rights, compliance, or governance strengths.

- Position as an enhancer for incumbents, not a disruptor.

- Structure deals so your IP becomes the default.

Hybrid Channels

5. OEM / White-Label AI

Best For: AI that works best invisibly, powering someone else’s product.

Sometimes the fastest path to scale is powering another company’s product from behind the curtain. OEM or white-label distribution means your AI runs under another brand, often as a feature inside systems customers already trust. The trade-off: less visibility, more reach.

As one investor framed it: “The best distribution is when customers don’t even know they adopted AI — they just see their system getting better.”

Case Study: Nuance → Epic Systems.

Epic dominates U.S. hospital EHRs (Electronic Health Records), but doctors were drowning in documentation. Nuance, a leader in speech recognition and medical transcription (now owned by Microsoft), embedded its Dragon Medical ambient AI directly into Epic. Doctors opened Epic and found notes auto-generated from their patient conversations.

By 2024, over 150 hospitals and health systems were using the technology, supporting millions of ambient encounters (AI that listens in the background and documents visits) annually. Epic owned the rail; Nuance supplied the intelligence. Together, they turned a point solution into a default workflow.

Keys to Success:

- Target platforms with deep industry penetration.

- Package AI as invisible, reliable infrastructure.

- Trade brand recognition for guaranteed scale.

6. Developer / API-Led GTM

Best For: Products — AI or otherwise — that can spread bottom-up through developers.

When procurement is slow, developers can become the distribution channel. If an engineer can plug in your API or SDK in an afternoon, usage spreads before formal approvals. Eventually, leadership supports what’s already embedded.

Product-growth strategist Lenny Rachitsky has highlighted how bottom-up, product-led adoption often outpaces traditional enterprise sales, particularly when developers can deploy solutions quickly and organically.

Case Study: LangChain → GitHub, Replit, & Others.

LangChain is an open-source framework for building apps powered by large language models. Instead of courting CIOs, it equips developers with LEGO-like building blocks: libraries, integrations, and templates. LangChain seeded tutorials and starter projects across GitHub — a widely used platform where developers share and collaborate on code — and amplified them through Twitter and YouTube.

Replit, an online coding environment that lets developers build and deploy applications entirely in the browser, integrated LangChain templates with one-click deployment. Developers could spin up LLM-powered apps in minutes — no infrastructure setup, no approvals, no sales process.

What began as hobby projects and experiments quickly became internal tools and prototypes inside real enterprises. LangChain didn’t need sales decks — frictionless deployment plus community adoption became the distribution engine.

Keys to Success:

- Deliver value in minutes (“first magic moment”).

- Seed adoption with repos, tutorials, templates.

- Create a clear path from hobbyist → team → enterprise.

Consumer-Focused Channels

7. AI-SEO / Answer Engine Optimization

Best For: Consumer-facing brands that need visibility in the AI “answer layer.”

Search is shifting from links to answers. If your product isn’t cited in ChatGPT, Gemini, or Perplexity, you risk becoming invisible at the moment of discovery. Just as companies once optimized for Google SEO, they now face Answer Engine Optimization (AEO).

The playbook: At a minimum, structure your data so LLMs can see, trust, and cite it. But the real leverage comes from going deeper — partnering directly with the platforms. Just as app developers compete for premium placement in app stores, brands can work with answer engines to secure preferred or featured positions. That might mean integrations with ChatGPT or Gemini, or making your API the default source for domain-specific questions.

Case Study: Zillow → ChatGPT.

Zillow — a leading real estate search platform — partnered with OpenAI to launch one of the first real estate experiences inside ChatGPT. Instead of relying solely on traditional search traffic, Zillow became part of the conversational interface itself.

Users can now ask questions like “Show me homes for sale in Seattle with a view” and get listings directly in the chat. Zillow’s data powers the response, making it the default source at the moment of intent.

Keys to Success:

- Treat LLMs as distribution channels.

- Structure data and content for ingestion and citation.

- Build partnerships to secure preferred placement.

8. Community-Led or Viral Growth

Best For: Consumer AI tools where sharing drives growth.

In consumer AI, distribution often looks like virality. When users share AI-generated outputs — images, audio, memes, or videos — those creations are the marketing. Each time someone remixes or personalizes an output, it reaches new audiences and spreads the product further.

As Sequoia put it: “Remixability is a distribution strategy. A template that spreads on TikTok can outperform a paid GTM plan.”

Case Study: Adobe Firefly → TikTok / Instagram.

Adobe launched Firefly, its AI image generator, inside Creative Cloud — its suite of tools like Photoshop and Illustrator. Designers began experimenting, and Firefly content rapidly spread through social networks, building demand even before its enterprise rollout. By the time Adobe rolled Firefly into enterprise licenses, demand was already primed socially.

Keys to Success:

- Design outputs to be remixable and shareable.

- Seed adoption in communities, not just campaigns.

- Let virality prime enterprise demand.

Conclusion — Platform Leverage Without Over-Dependence

Across all eight channels, the pattern is unmistakable: AI distribution flows through platforms. Cloud providers, SaaS ecosystems, GSIs, OEMs, developer communities, consumer networks, and industry incumbents increasingly control how AI reaches customers.

In many ways, these platforms are more than digital marketplaces — they’re the trucks, routes, and retail shelves of the AI economy. They don’t just control where customers look; they control how products get there in the first place. A few companies own the distribution infrastructure. Everyone else is trying to get on their delivery routes.

This is both an opportunity and a risk. Platforms can shrink sales cycles from months to days, open doors to customers you could never reach directly, and turn procurement rails into growth engines.

But the same platforms are structurally incentivized to compress vendor margins, subsume successful features, or reroute value capture back to themselves. They can also change the rules overnight — shifting APIs, pricing, or ranking algorithms.

Winning means not just capturing channels now, but adapting as they evolve.

The strategic challenge is balance:

- Ride distribution rails to scale faster than you could alone.

- Build moats platforms can’t easily copy: proprietary data, domain expertise, embedded workflows, network effects, or a trusted brand in high-stakes environments.

The companies that endure will treat platforms as accelerants, not foundations. They will partner, embed, and integrate — but never cede all leverage.

In the AI era, the smartest companies master platform channels to scale, while building their own moats so distribution accelerates them without owning them.

What this Means for Leaders

- Treat platform channels as accelerants, not anchors. Use cloud, SaaS, developer, and consumer platforms to scale faster — but don’t depend on any single partner for survival.

- Build moats that platforms can’t easily replicate. Proprietary data, domain expertise, embedded workflows, network effects, or trusted brands create durable leverage.

- Layer channels strategically. Winning AI companies don’t rely on one rail; they combine multiple channels to reach customers, compound distribution effects, and reduce platform risk.

- Continuously rebalance. Platforms evolve. Revisit your channel mix regularly as incentives, APIs, and economics shift.

About the Author

Tyler Moynihan is a technology executive with two decades of experience across AI, platforms, strategy, and M&A, including leadership roles at Zillow. He writes Tech, Systems & Power to explore how technology reshapes systems of power and real-world outcomes.

The Missing Piece of Your AI Strategy: Distribution was originally published in Towards AI on Medium, where people are continuing the conversation by highlighting and responding to this story.