Oracle Is Firing 30,000 People to Pay for AI It Hasn’t Built Yet

If your company is “pivoting to AI,” your job might be funding the pivot.

On February 27, 2026, OpenAI closed the largest private funding round in history: $110 billion, backed by Amazon, Nvidia, and SoftBank. Six days later, Oracle confirmed it would cut thousands of workers to manage what Bloomberg called “a cash crunch from a massive AI data center expansion effort”.

One company raised more money than the GDP of Morocco. Another began firing the population of a small city to keep the lights on for it.

$110 billion raised. 30,000 jobs cut. Same week. Same industry. Same story, told from two different floors of the building.

The Week That Cracked the Story Open

Three signals landed in the same week. The record fundraise. The mass layoffs. And a third event that almost nobody noticed.

On March 6, Reuters reported that Oracle and OpenAI had scrapped plans to expand their flagship AI data center in Abilene, Texas. Financing fell apart. OpenAI quietly shifted its near-term computing needs to Microsoft and Amazon instead.

The physical monument to Oracle’s AI ambitions got shelved because the money wasn’t there to pour the foundation.

And tucked into the court records from January: the Ohio Carpenters’ Pension Plan had filed a class-action lawsuit alleging Oracle concealed plans for $38 billion in additional borrowing just seven weeks after selling them $18 billion in bonds. Retired carpenters from Ohio, losing money on bonds sold to finance servers that will train AI models that might, eventually, replace carpenters.

That’s not irony. That’s the supply chain.

What Oracle Actually Said (And What It Meant)

Bloomberg’s reporting contained two explanations buried in the same story. Explanation one: some roles were being eliminated because “the company expects it will need less of them due to AI”. You’ve seen that headline a hundred times.

Explanation two sat one paragraph lower. The primary driver: a “cash crunch from a massive AI data center expansion effort”.

Those are different stories. Completely different. The first is about technology replacing labor. The second is about money replacing labor.

The humans aren’t being outperformed by software. They’re being liquidated to fund hardware.

Investment bank TD Cowen put the numbers on it. Oracle may cut 20,000 to 30,000 employees, roughly 18% of its 162,000-person workforce, to free up $8 billion to $10 billion in cash flow.

Do the division: each employee is worth roughly $330,000 to $500,000 in freed liquidity. Not as a worker. As a line item to be converted.

Oracle isn’t converting jobs into AI. It’s converting jobs into kilowatt-hours and GPU leases.

TD Cowen’s note didn’t soften it: “Both equity and debt investors have raised questions regarding Oracle’s ability to finance this buildout”. Banks have pulled back. Borrowing costs have roughly doubled since September.

The capex required to fulfill just the OpenAI contract? $156 billion.

The Money Math That Broke the Company

$156 billion.

Sit with that for a second. That’s what TD Cowen estimates Oracle needs in capital expenditure to deliver on one contract: a five-year, $300 billion deal to supply OpenAI with computing power. Three million GPUs. The contract that was supposed to turn a legacy database company into an AI infrastructure titan.

To start funding it, Oracle sold $18 billion in bonds on September 25, 2025. The prospectus told buyers Oracle “may” need additional financing. Seven weeks later, Oracle came back for $38 billion more in loans.

The Ohio Carpenters’ Pension Plan sued. Their argument was simple: Oracle wasn’t uncertain about future borrowing when it wrote “may.” The next tranche was already in motion.

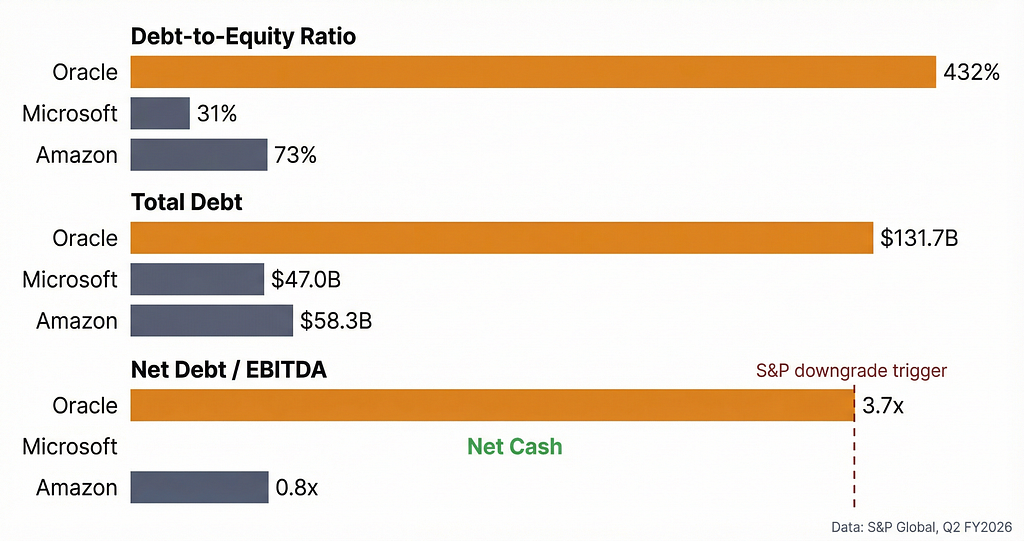

The bond market’s verdict arrived fast. Credit spreads doubled from roughly 50 basis points to over 130, the widest since 2009. Total debt hit $131.7 billion by Q2 FY2026, up from $99.5 billion a year prior.

The comparison that tells the story: Oracle’s debt-to-equity ratio sits at 432%. Microsoft’s is 31%. Amazon’s is 73%.

Same industry. Same AI buildout race. Completely different balance sheets.

Oracle is not in the same financial universe as its peers. It carries more than four times its equity in debt. The spending hasn’t peaked.

Morgan Stanley analyst Keith Weiss projects $275 billion in cumulative capex from FY2026 through FY2028, nearly $90 billion above what Wall Street consensus had modeled. He cut his price target from $320 to $213.

Three words in his note landed harder than the numbers: “Little room for error.”

Oracle’s free cash flow turned negative in Q3 FY2026 and, according to analyst estimates, will not recover until approximately 2029. The company already cut an estimated 10,000 jobs in late 2025 under a $1.6 billion restructuring plan. The new cuts would triple that toll. And the Stargate data center in Abilene that was supposed to justify all of it just got canceled.

When your company fires you and calls it “AI transformation,” check the 10-K. If free cash flow is negative and debt is at 432% of equity, you weren’t replaced by a machine. You were sacrificed to a balance sheet.

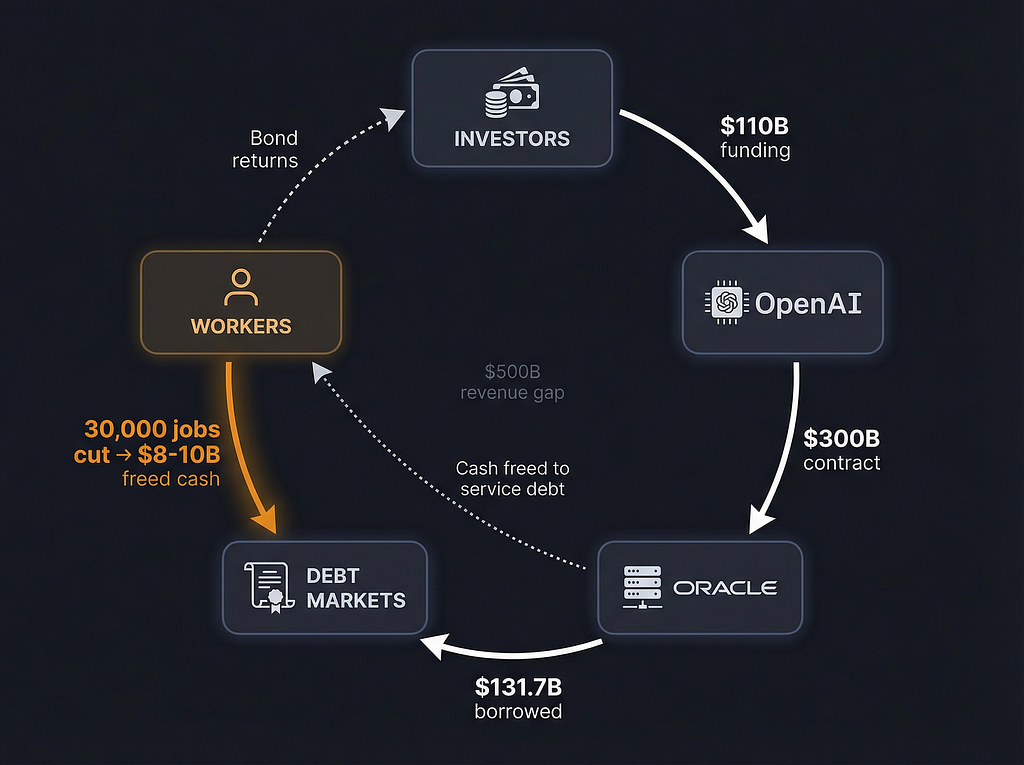

The Closed Loop

Follow the money. It moves in a circle.

OpenAI raises $110 billion from investors. OpenAI pays Oracle to build data centers. Oracle borrows to build them. Oracle fires people to service the debt.

Investors fund OpenAI because they believe AI revenue will materialize.

Repeat.

Sequoia Capital partner David Cahn spotted the math problem at the center of this loop in 2024. It has gotten worse since. The gap between what the AI industry spends on infrastructure and what it earns in revenue ballooned from $125 billion to $500 billion annually. His question still hangs in the air: “Where is all the revenue?”

You’re probably thinking: “But OpenAI’s revenue is growing fast.” It is. $20 billion annualized in 2025, up from $6 billion the prior year. Real growth.

But the company projects it needs $280 billion by 2030 and plans to spend $600 billion on compute to get there. That’s 14x growth in five years. Meanwhile, the vast majority of enterprise AI pilots still fail to produce measurable business returns. The companies buying AI infrastructure haven’t proven they’ll pay at the scale this machine requires.

The money is moving in a circle. The only thing leaving the circle is the workers.

The Canary, Not the Flock

Oracle’s crisis is severe. The pattern behind it is not unique.

Goldman Sachs estimates hyperscaler capital expenditure will exceed $600 billion in 2026. That figure has climbed every quarter for two straight years. The labor squeeze tracks alongside it: more than 176,000 tech workers lost their jobs in 2025 while AI infrastructure budgets swelled 46%.

Bain & Company’s 2025 technology report spells out the systemic math. For AI infrastructure spending to sustain itself, the industry needs roughly $2 trillion in annual revenue by 2030.

Even the optimistic scenario leaves an $800 billion annual shortfall. That gap is the macro version of Oracle’s company-level problem.

The spending is real. The revenue is projected. The distance between those two words is where careers go to die.

Every infrastructure boom in history has produced the same pattern: the people who build the railroad are never the people who ride the train.

The telecom buildout of 1998 to 2000 rhymes. Telecom companies spent more than $100 billion on fiber optic cable. Level 3 Communications’ stock dropped 95%. Much of the fiber sat dark for over a decade.

Goldman Sachs notes that AI capex currently sits at 0.8% of GDP; the telecom peak hit 1.5%.

That comparison cuts both ways. The ceiling is higher than today’s spending. But the floor under Oracle has already cracked, and we’re only at the halfway mark of the cycle.

The Bull Case (And Why It’s Half Right)

The counterargument deserves a fair hearing. Goldman Sachs maintains this is a supercycle, not a bubble. Hyperscaler balance sheets are genuinely stronger than what telecom companies carried in 1999.

The internet did eventually justify the fiber. Just not on the timeline the builders needed to survive.

Guggenheim still rates Oracle a Buy at $400, calling customer concentration concerns “blown out of proportion”. Oracle’s cloud infrastructure business grew 66% year over year in Q2 FY2026, and GPU revenue surged 177%. Demand is real. Growth is real.

But “the industry is fine” and “Oracle is fine” are two different claims. Microsoft sits on net cash. Amazon runs at 0.8x net debt-to-EBITDA.

Oracle carries $131.7 billion in debt, a 432% debt-to-equity ratio, and a class-action lawsuit from its own bondholders. Industry averages don’t save individual companies. Ask Level 3.

The Balance Sheet Test

The next time your company announces “AI-driven restructuring,” ignore the press release. Run three questions instead.

One: Is free cash flow positive or negative? If capex outstrips operating cash, the company is borrowing to build. Those layoffs aren’t about efficiency. They’re about staying solvent.

Oracle’s free cash flow won’t turn positive until roughly 2029, according to analyst estimates.

Every job cut between now and then converts a person into a debt payment.

Two: Is headcount shrinking while debt is growing? Workers out, borrowing up. That’s the signature of a liquidity event wearing a strategy costume. Oracle cut thousands of jobs and added $38 billion in new loans in the same quarter.

The AI industry’s dirty secret in 2026: the robots aren’t taking your job. The debt your company took on to buy the robots is.

Three: What’s the capex-to-revenue ratio? North of 45% means a company is building for a future that hasn’t shown up yet. Bain says the industry needs $2 trillion in annual revenue by 2030 and remains $800 billion short.

If enterprise AI adoption doesn’t accelerate hard in the second half of 2026, the correction begins with the most leveraged players and burns inward. That ratio is the single number that separates a boom from a burial.

They’ll build the data centers. They might even fill them. But the 30,000 people who paid for the concrete and the copper and the cooling systems won’t be there to see it.

Oracle Is Firing 30,000 People to Pay for AI It Hasn’t Built Yet was originally published in Towards AI on Medium, where people are continuing the conversation by highlighting and responding to this story.